Paid Sponsorship From Public: Receive a Free Stock Valued Up To $1,000 when you open an account and make a deposit! Go to http://public.com/graham and use code GRAHAM | Add me on Instagram: GPStephan

GET MY WEEKLY EMAIL MARKET RECAP NEWSLETTER: http://grahamstephan.com/newsletter

The YouTube Creator Academy:

Learn EXACTLY how to get your first 1000 subscribers on YouTube, rank videos on the front page of searches, grow your following, and turn that into another income source: https://the-real-estate-agent-academy.teachable.com/p/the-youtube-creator-academy/?product_id=1010756&coupon_code=100OFF - $100 OFF WITH CODE 100OFF

THE HOUSING MARKET:

Redfin just reported that “the median U.S. home sale price fell 3.3% in March, to $400,528” - which, was the largest year-over-year drop since 2012.

This is just the AVERAGE throughout the entire country, which means - other areas are seeing SUBSTANTIALLY WORSE declines - for instance, Boise Idaho has fallen 15.4% from a year ago with 78.8% fewer pending home sales, Austin, Texas is down 13.7%, Sacramento is down 11.9%, San Jose is down 10.5%, and, Oakland is down 9.7%.

NEW MORTGAGE FEES:

A new rule was announced that would “force homebuyers with good credit scores to pay higher mortgage rates and fees to subsidize those with riskier credit ratings who are also buying houses.” Although, in order to understand what’s going on, you first need to familiarize yourself with a term called “Loan Level Price Adjustments.”

These were introduced 15 years ago, after the mortgage crisis, to compensate for risks associated with lending money. In January of this year, NEW changes were put in place in an effort to level the playing field between those with GOOD CREDIT and those with BAD CREDIT - and, starting May 1st, the biggest discounts will be given to those with BAD CREDIT.

Here is the BEFORE / AFTER:

https://singlefamily.fanniemae.com/media/33201/display

https://singlefamily.fanniemae.com/media/9391/display

The largest changes really come from those with good, but not GREAT credit, in between 700 and 780 - and, this heat map really shows who’s paying the most:

https://a.mortgagenewsdaily.com/assets/63c9a2932026a02d6ca2665a/63c9a2932026a02d6ca2665a.png

Keep in mind, those with BAD CREDIT still pay more in fees than someone with good credit - but, people with good credit now get less benefit than they did before, while those with bad credit no longer don’t need to pay as much.

THE DEBT CEILING:

The United States is quickly running out of money, at - at current estimates - this could happen as early as June 2023. In terms of what could happen, JP Morgan believes that “they expect the debt ceiling to become an issue as early as May, and that the debate over both the ceiling and the federal funding bill would run "dangerously close" to final deadlines.”

As the New York Times pointed out, “breaching the debt limit would lead to a first-ever default for the United States, creating financial chaos in the global economy. It would also force American officials to choose between continuing assistance like Social Security checks….and paying interest on the country’s debt."

Let me know what you think about this in the comment sections - or, if you're actually reading this (I have no idea who actually makes it this far down), feel free to comment 'LOBSTER.' It'll be totally random and no one will have any clue what you're talking about - but, it'll be our little secret. Thanks!

My ENTIRE Camera and Recording Equipment:

https://www.amazon.com/shop/grahamstephan?listId=2TNWZ7RP1P1EB

For business inquiries, you can reach me at graham @night.co

*Some of the links and other products that appear on this video are from companies which Graham Stephan will earn an affiliate commission or referral bonus. Graham Stephan receives cash compensation from Public for sponsored advertising materials. Graham Stephan is part of an affiliate network and receives compensation for sending traffic to partner sites. The content in this video is accurate as of the posting date. Some of the offers mentioned may no longer be available. This is not investment advice. Public Offer valid for U.S. residents 18+ and subject to account approval. There may be other fees associated with trading. See Public.com/disclosures/

GET MY WEEKLY EMAIL MARKET RECAP NEWSLETTER: http://grahamstephan.com/newsletter

The YouTube Creator Academy:

Learn EXACTLY how to get your first 1000 subscribers on YouTube, rank videos on the front page of searches, grow your following, and turn that into another income source: https://the-real-estate-agent-academy.teachable.com/p/the-youtube-creator-academy/?product_id=1010756&coupon_code=100OFF - $100 OFF WITH CODE 100OFF

THE HOUSING MARKET:

Redfin just reported that “the median U.S. home sale price fell 3.3% in March, to $400,528” - which, was the largest year-over-year drop since 2012.

This is just the AVERAGE throughout the entire country, which means - other areas are seeing SUBSTANTIALLY WORSE declines - for instance, Boise Idaho has fallen 15.4% from a year ago with 78.8% fewer pending home sales, Austin, Texas is down 13.7%, Sacramento is down 11.9%, San Jose is down 10.5%, and, Oakland is down 9.7%.

NEW MORTGAGE FEES:

A new rule was announced that would “force homebuyers with good credit scores to pay higher mortgage rates and fees to subsidize those with riskier credit ratings who are also buying houses.” Although, in order to understand what’s going on, you first need to familiarize yourself with a term called “Loan Level Price Adjustments.”

These were introduced 15 years ago, after the mortgage crisis, to compensate for risks associated with lending money. In January of this year, NEW changes were put in place in an effort to level the playing field between those with GOOD CREDIT and those with BAD CREDIT - and, starting May 1st, the biggest discounts will be given to those with BAD CREDIT.

Here is the BEFORE / AFTER:

https://singlefamily.fanniemae.com/media/33201/display

https://singlefamily.fanniemae.com/media/9391/display

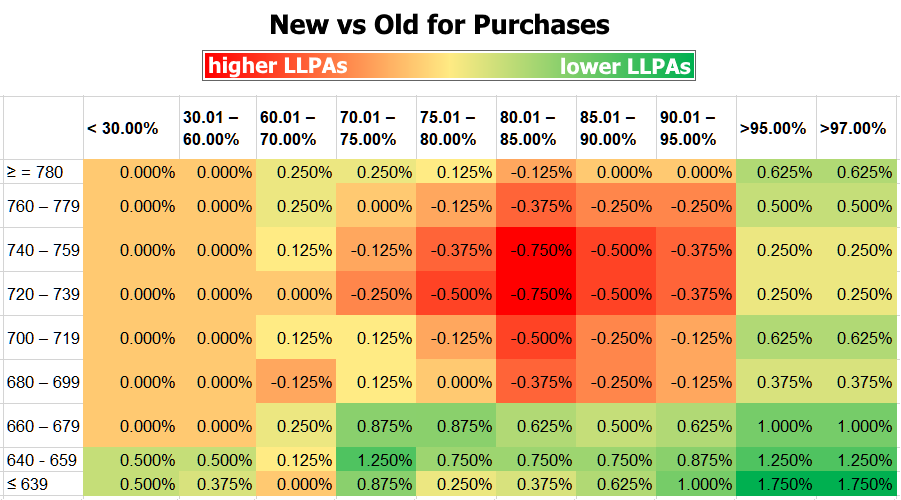

The largest changes really come from those with good, but not GREAT credit, in between 700 and 780 - and, this heat map really shows who’s paying the most:

https://a.mortgagenewsdaily.com/assets/63c9a2932026a02d6ca2665a/63c9a2932026a02d6ca2665a.png

{kind=link}

Keep in mind, those with BAD CREDIT still pay more in fees than someone with good credit - but, people with good credit now get less benefit than they did before, while those with bad credit no longer don’t need to pay as much.

THE DEBT CEILING:

The United States is quickly running out of money, at - at current estimates - this could happen as early as June 2023. In terms of what could happen, JP Morgan believes that “they expect the debt ceiling to become an issue as early as May, and that the debate over both the ceiling and the federal funding bill would run "dangerously close" to final deadlines.”

As the New York Times pointed out, “breaching the debt limit would lead to a first-ever default for the United States, creating financial chaos in the global economy. It would also force American officials to choose between continuing assistance like Social Security checks….and paying interest on the country’s debt."

Let me know what you think about this in the comment sections - or, if you're actually reading this (I have no idea who actually makes it this far down), feel free to comment 'LOBSTER.' It'll be totally random and no one will have any clue what you're talking about - but, it'll be our little secret. Thanks!

My ENTIRE Camera and Recording Equipment:

https://www.amazon.com/shop/grahamstephan?listId=2TNWZ7RP1P1EB

For business inquiries, you can reach me at graham @night.co

*Some of the links and other products that appear on this video are from companies which Graham Stephan will earn an affiliate commission or referral bonus. Graham Stephan receives cash compensation from Public for sponsored advertising materials. Graham Stephan is part of an affiliate network and receives compensation for sending traffic to partner sites. The content in this video is accurate as of the posting date. Some of the offers mentioned may no longer be available. This is not investment advice. Public Offer valid for U.S. residents 18+ and subject to account approval. There may be other fees associated with trading. See Public.com/disclosures/

What's up? Graham It's guys here and 2023 is already shaping up to be an absolute mess. Thieves have reportedly stolen 2 million dimes from the back of a van in Philadelphia a teenager was banned for climbing into and getting stuck in a claw machine and home prices just saw their largest annual drop in over a decade. Yep, you heard that correctly. Median sale price is absolutely plummeted in March market demand is abruptly Fallen another 10 percent and all of this comes at a time where a new provision would tax home buyers with good credit to lower costs for those with bad credit.

So with all of that going on, along with the fears of a looming debt crisis, it's important to understand exactly what's happening. where home prices are falling the most. Why? JP Morgan Warns that there's a risk of the United States defaulting on its debt for the first time ever in history and what you could do about this to potentially make money. On this episode of if you want to donate to charity, it's probably not a good idea to throw cash from a moving vehicle.

although before we go into that, as usual, if you appreciate all the research that goes, listen to making a video like this. It does help out tremendously. If you subscribe for the YouTube algorithm or if you want to be kept up to date on topics like this before, I'm able to make a full video. Feel free to check out my newsletter Down Below in the description.

So thank you guys so much And also big thank you to Public.com for sponsoring this video, but more on that later. All right now. First of all, when it comes to housing prices, this year is likely to be challenging for four main reasons: Number one is going to be interest rates. As you can see, mortgage rates have risen at their fastest Pace in history, and we're currently hovering around the same rates that we saw back in the early to mid 2000s.

Except, unlike 20 years ago, home prices are no longer a hundred and eighty seven thousand dollars. Instead, they're four Hundred thousand dollars. On top of that, 71 of homeowners and renters say that they will not accept the mortgage rate above five and a half percent, and as I'm sure you've seen right now, we're at 6.3 percent. The second people have less money.

A recent survey found that 61 of Americans will run out of emergency savings by the end of the year, and the majority have little to no retirement savings at all. In addition to that, almost 70 of those surveys said that they're now saving less money because of inflation, which basically means less money to spend than a home. A third, we have Rising layoffs. Yes, things aren't bad enough.

Layoffs have increased five-fold with tech companies leading the way. On top of that, jobless claims are also Rising with fewer people employed. And fourth, we have inventory. Surprisingly, housing inventory actually declined month over month with Buyers beginning to snatch up whatever's left on the market.

and since 2007, active listings have been on a steady downtrend as people lock in rates and then refuse to sell, keeping prices from falling further. All of that combined is leading to a rather volatile Market throughout the rest of the year. And in terms of what's happening now, you're going to want to hear this now in terms of how far home prices are falling: Redfin Just reported that the median U.S home sales price fell 3.3 percent march to four hundred thousand dollars, which was the largest year-over-year decline since 2012.. Now, keep in mind this is just the average throughout the entire country, which means that some areas are seeing substantial, actually worse to clients. For instance, Boise Idaho has fallen 15.4 percent, Austin Texas is down 13.7 percent, Sacramento is down 11.9 percent, and Oakland is down 9.7 pending. home sales also happen to be down across the board throughout the entire country, meaning buyers are making fewer offers, which is resulting in sellers having to readjust their price if they're expected to make a sale. In terms of what this means for you, practically speaking, 28 of U.S homes sold from more than their final list price in March, which is down from 54 from a year ago. Although even with prices continuing to fall, the majority of sellers are still refusing to list their home because that would mean giving up their existing mortgage for an even Higher One.

In fact, it's reported that 99 of homeowners have a rate below six percent, and the bulk of those are locked in under four percent, meaning prices would have to fall by 40 just for the monthly payments to equal the same cost as getting a higher mortgage should that person choose to move. Basically, Redfin is suggest testing that this is keeping the housing market from entering an utter free fall. and if something is priced well, you could still expect a bidding war depending on the location. However, this is only the very beginning because starting May 1st things are about to get a lot more expensive if you have a good credit score.

Let me explain. A few days ago, a controversial rule was announced that would force home buyers with good credit scores to pay higher mortgage rates and fees to subsidize those with riskier credit ratings who are also buying houses. Now if this sounds unbelievable, well that's because it is. And I Had a hard time wrapping my mind around where all of this originated since it seemed to have come out of nowhere.

So in order to understand what's going on, you need to familiarize yourself with the term called loan Level Price adjustments. These were introduced 15 years ago after the mortgage crisis to compensate for the risks of lending money. Basically, this allowed lenders to charge fees based on the likelihood that someone was not going to pay back their loan. Generally the lower the credit score, the higher the risk the borrower is and the higher the score, the lower the risk seems common sense, right? Well, in January of this year, new changes were put in place that would level the playing field between good credit and bad credit and starting May 1st the biggest benefits would go to those with bad credit. Of course, this inevitably winds up getting spun around is Biden redistributing high-risk loan costs to homeowners with good credit. which is kind of true, but it's not the entire picture just to show you a before and after. If you have a 640 credit score and put 25 down, you'd previously have to pay a fee of 2.75 percent. Now that same borrower will only have to pay a one and a half percent fee.

On the other hand, if you have a 750 credit score and put 25 down, you used to be charged to 0.25 fee and now you're going to have to pay a point three, seven, five percent fee unless your credit score is above 780. In which case, everything stays the same and this heat map really shows who's paying the most. As you can see, borrowers in the middle wind up paying 0.75 more than before, while borrowers in the lowest credit tiers see a marginal savings. Now don't get the wrong idea because people with bad credit still end up paying more in fees than people with good Credit but people with good credit now get less benefit than they did before and people with bad credit end up seeing a slight savings.

It's kind of like in really simple terms: if the house is a hundred dollars, a person with good credit would pay a dollar instead of paying 25 cents, and a person with bad credit would pay 2.85 cents instead of paying three dollars and 25 cents. If the Federal Housing Authority claims that this is to help maintain the Financial Health that Fannie and Freddie a key element to their responsibility is a conservative. but just like all things politics, they don't make a lot of sense. Like our next topic, Because mark my words, this is going to be a huge issue over the next few months.

However, before we go into that when it comes to investing, our Sponsorpublic.com wants to help because they're an investment platform that helps people be better investors. In fact, Public is the only investment platform that allows you to buy, hold or sell a wide variety of options all in one place from stocks ETFs fractionalized alternative Investments Fine arts, collectibles and more now including treasuries which gives you the option to earn a fixed return at competitive rates. Not to mention, with Public, these treasuries have no minimum hold periods or settlement delays, and they're securely held in custody. at the Bank of New York Mellon the world's largest custodian bank and Security Services Company This means the public could be your One-Stop shop to build a well-diversified portfolio within a platform that doesn't sell your trades to market makers like some of the other investment apps do.

They've also just recently launched Public Premium where you could view all the latest performance data, price targets, analyst reports, and more right from your desktop or phone. This also includes premium only content where you could listen to experts, break down the latest Market headlines, Trends, and news. And best of all, if you sign up and make a deposit with the code Graham you could get a free stock slice now worth all the way up to a thousand dollars when you use the link Down Below in the description. or if you go to Public.com Graham feel free to check out all the details down below to get started today. And now with that said, let's get back to the video. All right now in terms of what's Happening throughout the broader economy. As a country three, we are quickly running out of money and the current estimates indicate that that could happen as early as June, which as you could see is less than two months away. See, all of this comes down to What's called the debt Ceiling, which is the maximum amount of money that the United States is able to borrow to pay for all of its obligations like Social Security and Medicare benefits, military salaries, interest on the national debt, and a multitude of other services that the country needs to continue running.

However, once the debt limit is reached or we hit a ceiling, those items can no longer be funded to the point where they eventually have to begin cutting back and shutting down services to conserve their resources. It's really no different than someone running out of money in a bank account after maxing out all of their credit cards and then scrambling to come up with whatever they can to stay afloat. except this time it's the entire country. The go-to solution would be to Simply raise the debt limit and borrow more money to pay for everything, but that requires that both sides agree to the terms of the new debt, and if they don't it becomes like a game of chicken to see which side flinches first and you are the one that pays the price.

In this case, House Republicans Say that they'll support raising the debt ceiling if Democrats reduce their spending and eliminate student loan forgiveness, but Democrats say that they simply want to keep everything as is and raise the debt ceiling alongside with it in terms of what's probably going to happen. JP Morgan Believes that the debt ceiling is going to become an issue as early as May and that the debate over both the ceiling and the federal funding bill would run dangerously close to final deadlines. As a result, treasury bills, which are essentially loans to the US government are surging, signaling a higher risk that there's a very, very small chance that they can't agree on time and miss one of their debt deadlines, which would be disastrous. As the New York Times pointed out, breaching the debt limit would lead to a first ever default for the United States, creating Financial chaos in the global economy. Even though the United States has never defaulted on its debt in 2011, they got so close that the S P Credit Reporting Agency downgraded them from Triple A to double A Plus And so several other agencies issued a negative outlook as the debt crisis continued getting worse. Following that announcement, all three stock indexes fell between five and seven percent in a single day, and the President of the S P resigned shortly after. Now today, the market believes that there is a two percent chance of them not agreeing and defaulting on their debt, which unfortunately is the highest it's ever been. But all of this leads to what's being called The X date, which is simply the day the United States runs out of money and that is coming up way faster than any of us expected.

So in terms of what this means for you, there's really only three outcomes: number one, Democrats give in number two, Republicans given, or number three, which is most likely both sides will have to come together, give concessions, and work it out. On top of that, it's also worth mentioning that reaching this debt ceiling limit is not anything new, and it's been happening on a regular basis for the last hundred years. In fact, the last time this occurred was back in late 2021 when the government hit their debt ceiling limit of 28.4 trillion dollars and after months of deliberations, halting reinvestments and cutting spending, eventually they agreed on a new debt ceiling limit until that too ran out and they need to ask for more, which is where we are today now, even though the most likely scenario is that both sides spend a few weeks or months negotiating to Kick the Can further down the road in the unlikely event of a Black Swan case where they cannot agree on a budget and they end up missing a payment, The Fallout from a lower credit reporting would absolutely cause ripples throughout the entire market and would make it more expensive for the government to borrow money because all of a sudden they would no longer be risk-free or basically the stock market really doesn't care until things get really bad. Although in terms of what I think about all of this in terms of the debt ceiling.

Unfortunately, the entire situation has devolved into a political back and forth of various spending agendas, and I have a feeling they're going to get as close as possible to actually defaulting without actually defaulting, because that would be the equivalent of burning everything down for the sake of not letting the other person win. But once they agree on a new debt ceiling, chances are they're going to keep pushing the can further and further down the road until eventually. It's another generation's problem and we don't have to think about it now. in terms of the mortgage fee increases though, that one I have no clue about it really doesn't make a lot of sense to me to raise fees on those that are deemed less risky, but then again, nothing really makes sense anymore. That's why it's probably best that you subscribe and hit the like button, so that way it could be kept up to date on topics just like this and you don't miss out. So thank you so much for watching As always, feel free to add me on Instagram And as usual, don't forget that you could get a free stock with all the way up to a thousand dollars with our sponsor Public.com Down Below in the description when you make a deposit with the code Graham Enjoy! Thank you so much And until next time.

If the current value of my house falls 25 percent, then my property taxes will also go down 25 percent. Right?

Your wrong, Florida real estate never goes down lol.

Will it crash like FTX? Remember the coin you promoted and then it completely crashed 💥 that one. Will it crash like that one?

What is going on?

Socialism/Communism is happening right before our eres. We need to get rid of the foreign central banksters for good…. the irs.

This President has to go! Why I have to pay for someone with bad credit ???

The Feds has just unleashed chaos! I wonder if people that experienced the 2008 Housing crash had it easier because this market conditions are driving me to insanity, my portfolio has lost over $47000 this month. alone my profits are tanking and I'm don't see my retirement turning out well when I can't even grow my stagnant reserve.

The current system is completely unsustainable. The only reason it continues 'as if' is lending and debt. Lending for healthcare, for homes, for education, and plain old credit cards. trouble is, when the bottom falls out, the lenders get bailed out and consolidated, and everyone else loses their shirt.

All I can say is that I did the math, and with interest rates, I would throw away more money on interest in year if I bought a house, even with 20% down, than I would on rent for a house. And the cost difference between renting and a mortgage, I could put all of that and my down payment into a high yield CD for a chunk of time and make more money. My other choice is to buy a house in an area I really don't want to live in, but still, for that to work out, I'd have to live there for a long time, and I don't want to. I'd rather pay rent to be near my family while we wait for things to settle down. It's really sad though.

Biden destroyed America !

Whats up graham its guys here, dont you think for a minute I missed that. 😀

"What's up Graham, it's guys here" 😂

Always very important to know what we are dealing with 👍🏻

First sentence you said what up graham it's guys here. 😂

Get rid of rental property and that would go a long way to helping the economy. Renting is usury

This is a BS idea!

Your thumbnails make you look grifty

What are your thoughts on CBDC’s coming into play ?

it makes a lot of sense, ppl with good credit score are mostly middle class, the government is taxing middle class to cover the risky loan bets made by the wall street elites to the poors

“What’s up Graham, it’s guys here.” 😂😂😂

This is will simply cause people who have good credit to tank their credit on purpose right before applying for a mortgage. Anyone with a half functioning brain knows how to reversibly tank their score… Just take your lowest limit card to 100%, done deal, more than a hundred points down the drain, you simply pay it off after it's reported.

cut all military except for the nukes. That is where the money comes from. We have nukes. We do not need a military.

Really I didn't know if you're above 780 you don't have fees. I'm probably a couple points shy of 780 so that's good to know as if I get my credit up to 800 I'll be saving money.

That's some impressive choreography.

I respect your opinion, I don't see any crashes, of course prices has been down but not dramatically. Inflation keeps up, meaning that tools supply and raw material are more expensive, not to mention labor.

In other words, new houses are more expensive to build .

The only way the house prices crash is if the whole economy system goes down.

Banks system or a war.